Growing Household Debt Drags Down Savings of Indian Families

Representational Image.

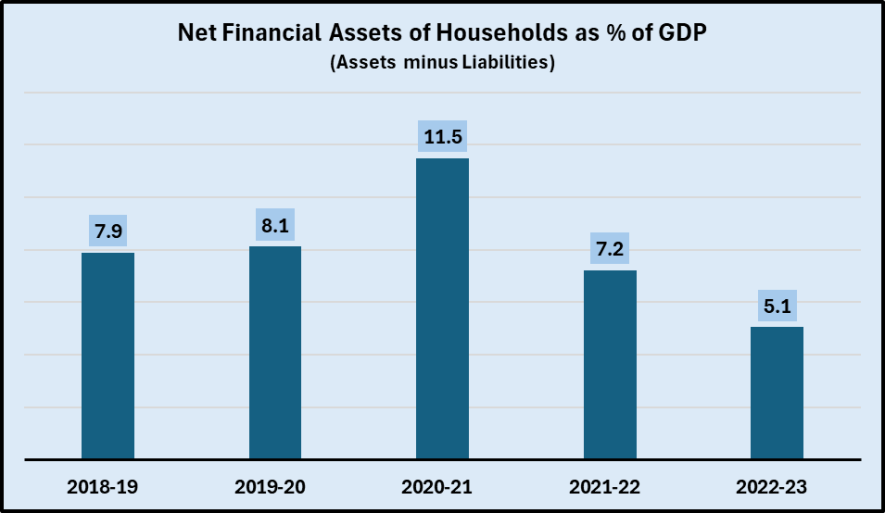

Net financial assets of households have sunk to just 5.1% of GDP (Gross Domestic Product) in 2022-23, according to latest data available from the Reserve Bank of India (RBI). As shown in the chart below, this is a five-year low and less than half of the level two years ago in 2020-21. These figures are only for financial assets, that is, bank and non-bank deposits, cash, investments in equity, insurance and pension funds, etc. The figures are net of liabilities, that is, liabilities like loans taken are deducted.

For most of the country’s citizens, financial assets are the main form of savings and thus a decline reflects mainly the dependence on savings in the face of low incomes, high inflation and the raging problem of unemployment. Families appear to be using savings for survival, or, as is more likely in the case of vast majority of people, not saving at all.

However, the picture is more complicated than this. In the same period, liabilities of households – mainly loans – have increased and thus, the net financial assets become less. Also, there is the possibility of people – at least the upper middle class and elite sections – opting to convert their savings into gold or silver, or buy physical assets like land or built houses. Let us look further into this.

Increasing Debt

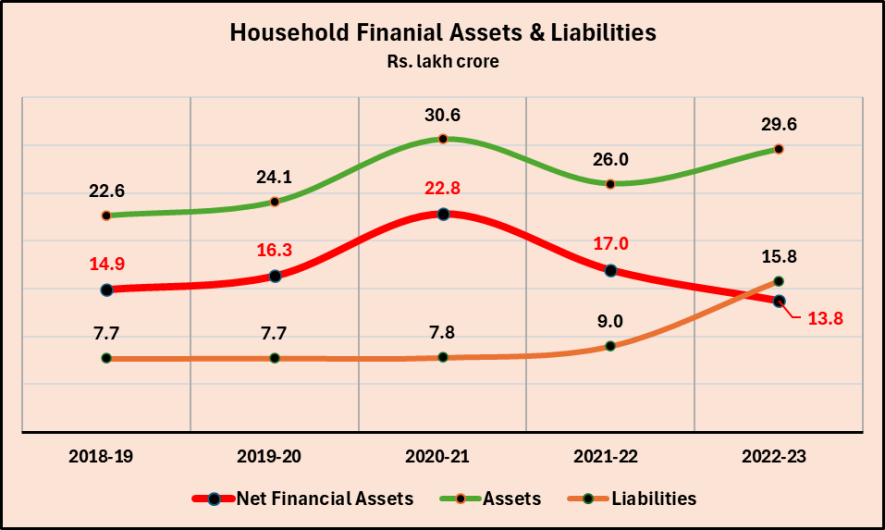

The chart below, derived from RBI data, shows the trend in household financial assets and liabilities over 2018-19 to 2022-23. In the first year of the pandemic, 2020-21, financial assets increased steeply to reach nearly Rs.31 lakh crore (green line) because the economy was mostly under lockdown and there were hardly any transactions taking place. What was in the banks or shares remained there. In the next year, there was a big dip as the economy stuttered back to life. Then, in 2022-23, assets further increased though remaining just short of the peak in 2020-21.

But now look at the liabilities shown in the orange line. There is an increase in 2021-22 coinciding with the reopening of economy. In 2022-23, liabilities zoom up to a jaw dropping level of Rs.15.8 lakh crore, more than half the level of assets/savings. People are increasingly becoming indebted. This causes their net financial assets (red line) to sharply decline to Rs.13.8 lakh crore.

Composition of Assets and Liabilities

What are liabilities made up of? The RBI data gives details: these exclusively consist of loans, mainly from banks (77% of all liabilities), with the remaining taken from Non-Banking Financial Companies (NBFCs), housing finance companies or insurance companies, etc. Liabilities have increased by over 26% per year over 2018-19 and 2022-23, indicating the increasing popularity/need of bank loans.

How are the financial assets held? Bank deposits make up about 35% of these assets, followed by provident and pension funds including PPF (22%), life insurance funds (18%), and small savings (excluding PPF) (7%). It is interesting to note that only about 7% of all financial assets are held in “investment” instruments – of which the bulk (6%) are in mutual funds and a mere 0.8% in equity (shares). This shows that it’s a very thin slice of Indian people that are investing in the share market, which however continues to hog the limelight and focus of both the government and the media.

Bank deposits have increased by about 9% per year in this period between 2018-19 and 2022-23, as have life insurance funds while provident and pension funds have grown by about 16% per year. Investments have increased by about 6% annually though the thin slice of investment in equity has rocketed up by over 65% per year, perhaps due to the spread of phone-based investment apps.

Gold/Silver and Real Estate

RBI also provides data for the estimated savings in both, gold and silver, and in physical assets, though the latest such data is for 2021-22. Savings in physical assets are estimated at nearly Rs.28 lakh crore, which is 107% of the total savings in terms of financial assets for that year. Savings in gold and silver are estimated at nearly Rs.60,000 crore, only about 2% of the savings in financial assets.

It must be mentioned that all the above figures are from officially recorded and legal transactions. There are vast amounts of funds and physical assets that are held through legal loopholes or even illegally, constituting the black economy. However, this kind of saving and assets can only be accruing and getting held by the well heeled or elite sections of population. As we know, just 1% of the richest Indians own about 40% of the country’s wealth while the bottom 50% own just 6.4% of the country’s wealth, according to latest estimates for 2022-23 by Thomas Piketty et al. published in the World Inequality Database (WID). It is inconceivable that anybody outside of the top 10% would either invest in real estate or precious metals, or hold significant amounts of black monies.

In other words, the declining net savings (as represented by financial assets) is a characteristic of the economic distress of the majority of common people. It is a direct result of the pro-rich policies of the present government and only the reversal of such policies can bring relief to people. The ongoing general elections can provide an opportunity to change these policies.

Get the latest reports & analysis with people's perspective on Protests, movements & deep analytical videos, discussions of the current affairs in your Telegram app. Subscribe to NewsClick's Telegram channel & get Real-Time updates on stories, as they get published on our website.