Banking: Deposit Competition & Funding Stress

Representational image. Image Courtesy: The Blue Diamond Gallery

Suddenly, every bank wants your deposit. Special FD (fixed deposit) offers, higher rates, and flashy campaigns flood the market. To citizens, this looks like generosity. In reality, it is survival — a scramble for funds as lending outpaces saving.

What appears to be a gift to depositors is actually the first signal of imbalance. To understand why, we must look at the numbers.

Diagnosis – The Numbers Behind the Stress

Reserve Bank of India (RBI) data shows that credit growth has surged to ~14.6% yearonyear, while deposit growth lags at ~12.5% . As a result, the LoantoDeposit Ratio (LDR/CD ratio) has climbed to an alltime high of ~82%, well above the healthy 70–75% range that normally signals balance.

This imbalance forces banks to lean on wholesale borrowings, Certificates of Deposit, and shortterm funding to sustain loan growth — a fragile foundation that magnifies liquidity risk.

But this imbalance is not abstract. It touches citizens directly:

- Depositors face tighter competition for funds, potentially higher deposit rates, and vulnerability if liquidity stress escalates.

- Borrowers encounter aggressive loan pushes, but also risk higher interest costs if funding strains persist.

Citizen Impact – How It Touches Everyday Lives

Depositors are being tempted by banks offering higher FD rates and flashy shortterm schemes. On the surface, these look attractive, but many come with hidden lockins or unsustainable terms. Ordinary savers risk chasing returns that may ultimately erode their financial flexibility.

Borrowers, meanwhile, are feeling the pinch as loan costs rise. Banks, under funding stress, pass on the burden through costlier EMIs. In their rush to meet lending targets, underwriting standards weaken, leaving households vulnerable to debt traps.

Banks themselves are caught in a squeeze. Loan growth is racing ahead of deposit growth, forcing them to rely more on wholesale borrowing. With weak CASA (current account/ savings account) inflows, this imbalance creates funding stress, margin compression, and liquidity risks that ripple through the system.

Regulators like RBI are monitoring these imbalances, but disclosure remains limited. Citizens are left unaware of systemic fragility, and policy signals often arrive late, weakening trust in the system’s resilience.

Government and policymakers, meanwhile, celebrate credit expansion as a sign of growth. Yet, in doing so, they neglect the deposit culture that underpins household savings. This neglect worsens systemic imbalance, leaving citizens caught between attractive offers and hidden risks.

To understand why banks are under such pressure, we must look at the drying oxygen of banking — CASA deposits.

CASA Pressure – Why Cheap Funding Is Drying Up

RBI’s Handbook of Statistics on the Indian Economy (2025) shows household financial savings as a share of GDP (gross domestic product) have halved in recent years, with a marked shift away from traditional bank deposits into mutual funds, equities, and fintech wallets.

At the same time, RBI data confirms that the share of household term deposits fell to 45.8% in FY2025, down from over 50% in 2020, as savers chased higher yields in capital markets. This erosion of lowcost CASA deposits is squeezing banks’ margins and raising liquidity stress.

With CASA weakening, banks are forced to rely on costlier term deposits and wholesale borrowings to fund loan growth. In turn, they chase lending even harder — and this overzealous push is a warning sign that the entire financial system is becoming more vulnerable, with thinner safety buffers and greater risk for ordinary depositors and borrowers alike.

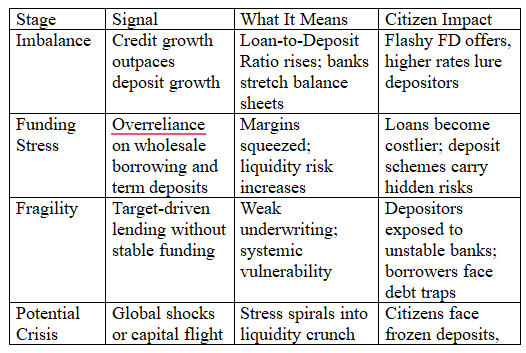

Overzealous Lending – Target-Driven Growth

Bank boards chase loan growth targets to signal expansion. Lending beyond deposit capacity is imbalance, not progress. Overzealous lending without stable funding is a warning signal of systemic fragility – as shown in the table below:

India is not alone in this pattern. Global crises show how deposit competition can spiral into collapse.

Global Parallels – Lessons from Abroad

The US and European crises were amplified by deposit competition. India’s current phase mirrors this pattern: strong credit demand, weak deposit inflows, rising funding stress.

If the signals are clear, then accountability must be asked: who is responsible?

- Bank Boards: chasing targets, neglecting deposit mobilisation.

- RBI: monitoring but opaque, slow to act.

- Government: celebrating loan growth while ignoring deposit culture.

Citizens are caught in the middle.

If institutions are failing, citizens must protect themselves. That requires a toolkit.

Citizen Toolkit – How to Spot Stress Signals

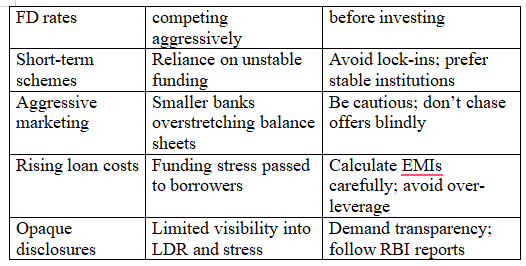

Red flags include unusually high FD rates, short-term schemes, and aggressive marketing by smaller banks. Citizens must avoid chasing rates blindly and check sustainability.

Citizen Toolkit Checklist:

Citizens can act, but systemic reform is also needed.

Reform Mandates – What Needs to Change

- Transparent LDR Disclosure: RBI must publish loantodeposit ratios (LDR) regularly so stress signals are visible early.

- Deposit Scheme Accountability: Banks should clearly disclose lockins, risks, and true costs of FD offers.

- Strengthen Household Deposit Culture: Policy must encourage stable savings in deposits, not just celebrate loan growth.

- Citizen Safeguards: Introduce consumerprotection norms to shield depositors and borrowers from unsustainable schemes.

Ultimately, the imbalance is a warning signal — and ignoring it risks fragility.

The Warning Signal

India’s banks are lending faster than they are saving. Deposit wars are not competition — they are stress signals. Overzealous lending without matching deposits is imbalance, and it is a warning sign of systemic fragility.

What looks like generosity is survival. What looks like growth is imbalance. If regulators and boards keep celebrating loan expansion while deposits dry up, citizens will discover too late that the gift was a trap — and the trap was systemic fragility.

The writer is a CAIIB (Certified Associate of the Indian Institute of Banking and Finance), has 37 years of experience in the private sector and a nationalised bank. He is ex-All India Deputy General Secretary of All India Bank Officers’ Confederation. The views are personal.

Get the latest reports & analysis with people's perspective on Protests, movements & deep analytical videos, discussions of the current affairs in your Telegram app. Subscribe to NewsClick's Telegram channel & get Real-Time updates on stories, as they get published on our website.